Planning an Audit of Oversight of a Public Agency, Board or Authority

This section of the Practice Guide is organized according to the key actions and decisions that need to be made during the planning phase of the audit process:

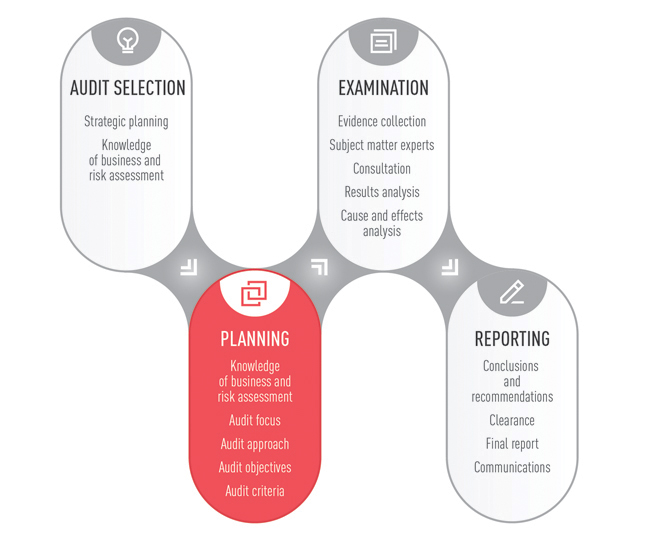

- Acquiring knowledge of business and assessing risk

- Determining the audit approach

- Drafting audit objectives

- Selecting audit criteria

Although these topics are presented in a specific order, planning a performance (value-for-money) audit is rarely a linear process. In fact, the planning process is often iterative, with decisions in one step requiring the audit team to review decisions made in previous steps to ensure the audit plan’s overall coherence.