Introduction to Auditing Oversight

Audits of oversight follow the same standards and general process as all performance audits. Auditors are required to follow the standards and audit processes applicable to their body of practice and office mandate.

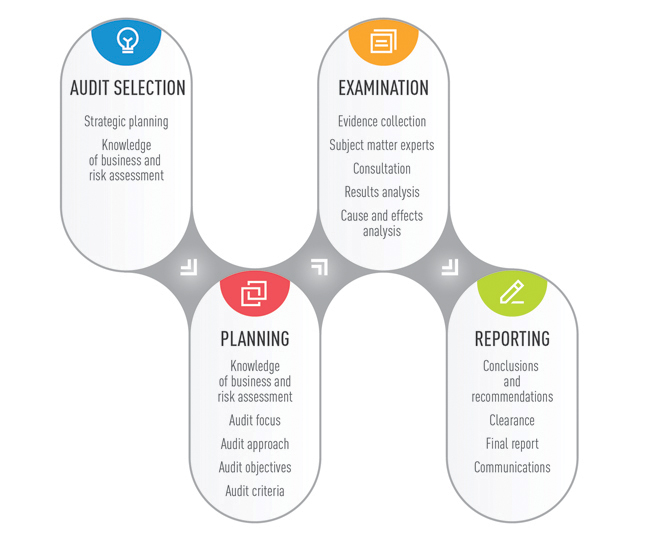

An overview of the generic audit process is in Figure 9.

Figure 9

Overview of the Performance Audit Process

The diversity of governance structures in any jurisdiction’s public sector and the diversity of oversight functions in any organization mean that auditors will rarely be able to apply the same audit plan to different organizations. However, auditors can apply a common methodology to plan all their audits of oversight.

When undertaking an audit of oversight, auditors will need to:

- select a significant oversight topic (for example, oversight of food safety, oversight of major capital projects) to audit and

- select one or more organizations to audit and develop a very good understanding (“knowledge of business”) of each audited organization’s governance structure, oversight responsibilities, strategic direction, and performance expectations.

Once these decisions are made, auditors will need to determine the extent of focus that the audit will place on oversight:

- Should the audit deal exclusively with oversight (that is, should it be a “stand-alone” audit of oversight) or should oversight be part of an otherwise broader performance audit where oversight is only one of the topics covered by the audit?

Auditors will also need to decide whether their audit approach will be to look at:

- the structures and systems of oversight bodies and functions or

- the results and effectiveness of these bodies and functions.

Alternatively, auditors could decide to combine both of these approaches in the audit in order to provide a more complete assessment of oversight responsibilities.

In addition to identifying the topic, focus, and approach of the audit, auditors will need to prepare a detailed audit plan that includes audit objectives, audit criteria, and audit procedures.

This Practice Guide provides information and guidance that will help auditors to complete the successive steps involved in planning, conducting, and reporting the results of an audit of oversight. This guidance will be especially useful to auditors who wish to audit:

- oversight of agencies, boards and authorities; and

- oversight of major initiatives in departments and ministries.

The Practice Guide also includes a glossary and a list of references (with hyperlinks to quickly access audit reports and other relevant documents on oversight).